Is this time different?

Is this time different?

A roaring '20s will require a much stronger economic recovery from Covid than from the global financial crisis. What are the chances?

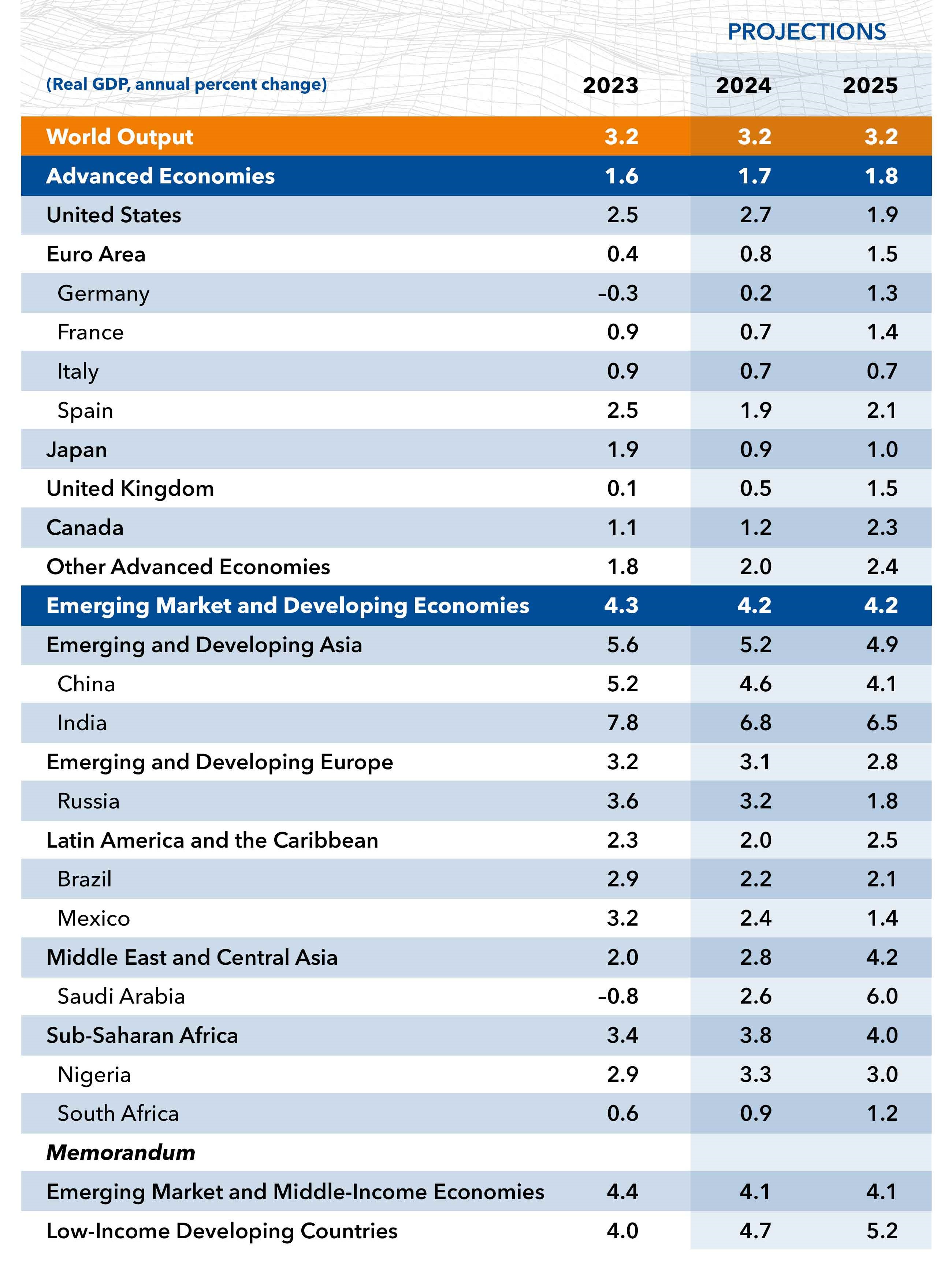

The IMF’s latest World Economic Outlook, released on Tuesday, marked up world GDP growth for 2024 by 0.1% relative to their January forecast, largely on the basis of stronger US growth. The US (2.7%) is expected to grow much faster than the EU (0.8%) and Japan (0.9%) in 2024, and to sustain a performance edge going forward. China held steady at 4.6% and 4.1% for 2023 and 2024 respectively.

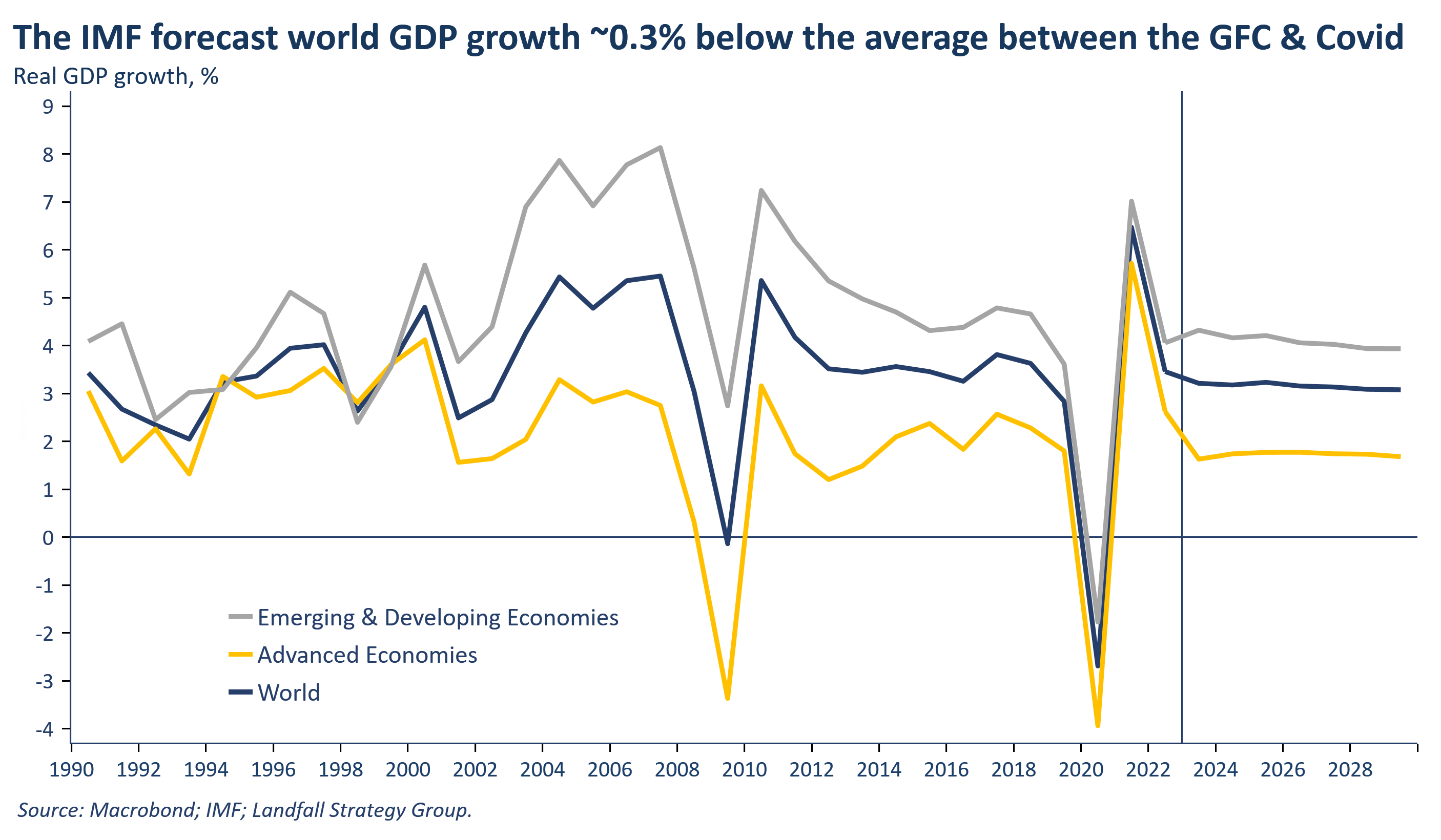

The last few IMF World Economic Outlooks have marked up growth forecasts. But the broader trend is down. World GDP growth is expected to average around 3.2% over the next several years, down ~0.3% from its average from 2011-2019. Growth rates across advanced economies and emerging markets are both expected to soften.

This weakening growth profile is consistent with historical trends. IMF analysis shows that the structural growth outlook has been weakening since the global financial crisis. The IMF’s 5-year ahead world growth forecasts have consistently declined since 2008 – and are now sitting at their lowest levels in decades.

This weakening outlook is partly a function of weakening labour force growth, but largely to weakening productivity growth. The IMF attribute this soft productivity performance to weaker allocative efficiency in the economy as well as to low levels of productive investment (despite the low interest rate environment). The IMF expect lower levels of investment and total factor productivity growth over the coming period, leading to a weaker global growth outlook.

IMF Managing Director Kristalina Georgieva gave a talk last week, expressing concern that this decade could turn into the ‘tepid 20s’ rather than the hoped for (roaring) ‘transformational 20s’. So how positive or negative on the economic outlook should we be?

Structural breaks

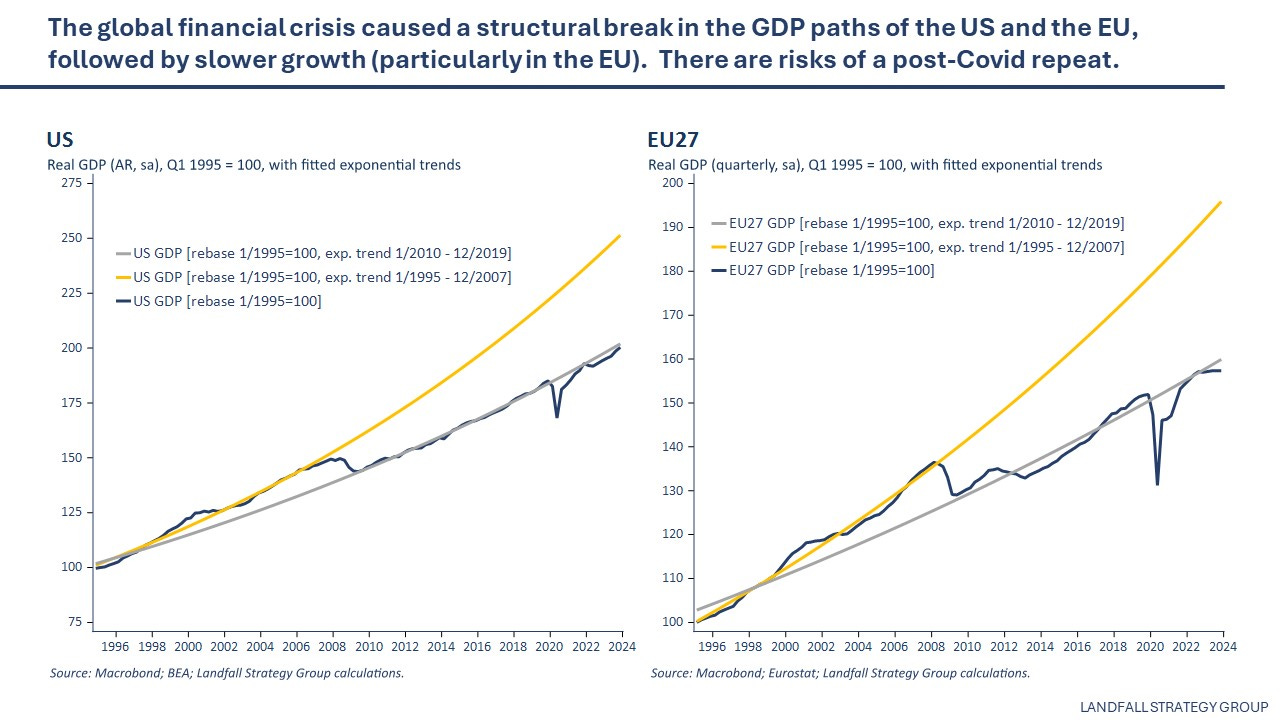

To think about the growth outlook over the next decade, it is useful to compare and contrast the current outlook with the post-global financial crisis experience. Across advanced economies (and beyond), the global financial crisis had a large, enduring effect on economic activity.

The global financial crisis caused a structural break in the path of GDP and labour productivity; these variables departed from trend, and took a few years to start growing again – and then at a slower pace. There was no convergence back to the pre-global financial crisis trend. The same pattern was observed across advanced economies, although with some national variation. This weak growth was particularly acute in the EU and the UK, where relatively contractionary macro policy was deployed (in contrast to the US, which recovered more strongly).

However, there was no meaningful structural policy response across advanced economies to the global financial crisis; the major policy innovation was quantitative easing and low/negative interest rates to respond to the demand-side shock. Little was done in large economies to strengthen trend productivity growth rates.

Similarly, the pandemic imposed substantial losses across economies. The economic recovery was much quicker than had been expected – due to the rapid deployment of effective vaccines, and also aggressive fiscal and monetary policy support.

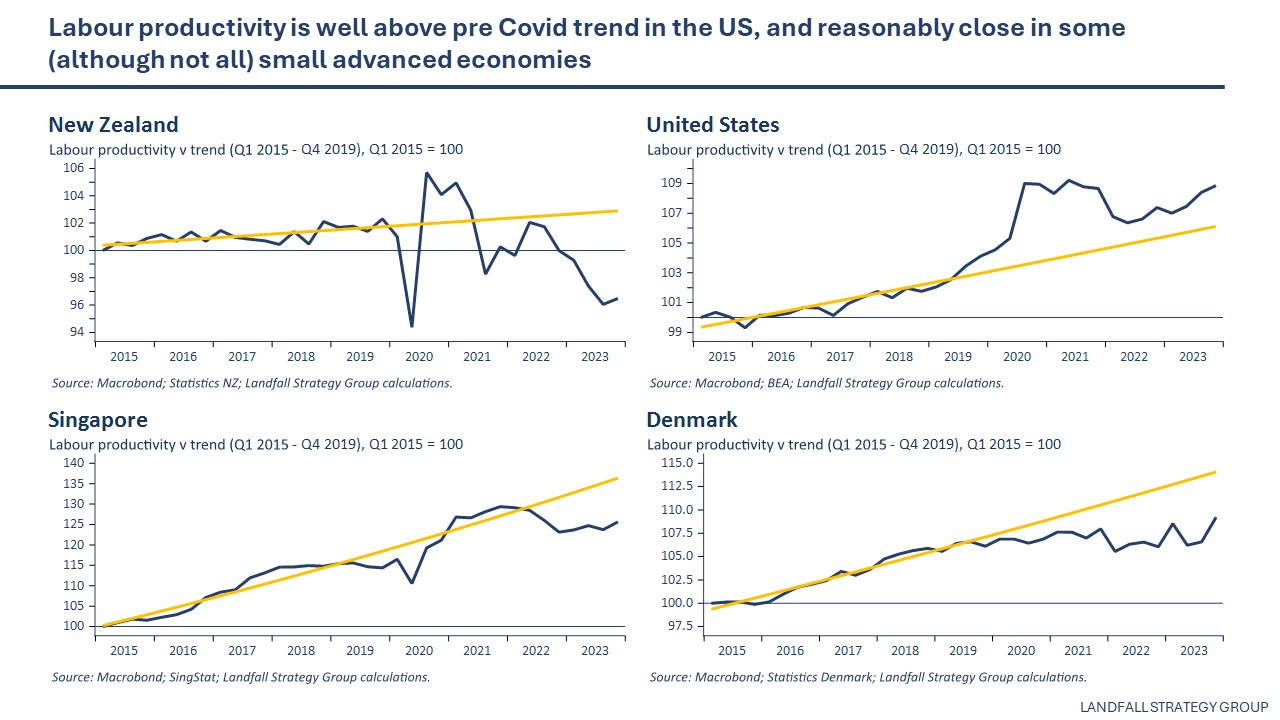

Even so, there was a significant economic hit. Although real GDP returned to its pre-Covid levels by the end of 2021 across most advanced economies, it has not recovered back to its pre-Covid trend. This departure is also apparent in terms of labour productivity; across advanced economies, only the US has returned labour productivity to its pre-Covid path.

This time is different?

In assessing the outlook for the decade ahead, a key question is whether the global economy will repeat the post-global financial crisis decade: a structural break in GDP and productivity performance, followed by weaker growth. Or whether, economies will be able to converge back to pre-pandemic paths of GDP and productivity – or indeed, exceed them.

It is too early to say much definitive. And there is substantial variation across advanced economies: the US is doing much better than the EU and the UK, for example. Across small advanced economies, economies thought to be disadvantaged in the emerging context, there is also variation: but on average, small economies continue to perform well – and are forecast to maintain a meaningful edge over larger economies over the next several years.

Of course, there are many structural challenges – which have been discussed frequently in these notes. For example, the growing frequency of economic and political shocks – from global supply chain disruptions to the economic impact of conflict on energy prices. And the increasing tendency for global economic fragmentation, as trade and investment flows are increasingly shaped by geopolitical rivalry – and by aggressive inward-looking industrial policy, will introduce costs and distortions into the global economy. A slowing China will also weigh on the global economic outlook.

On the positive side, fiscal policy has generally been more supportive of economic activity than was the case after the global financial crisis. Although public debt levels are worryingly high in many advanced economies, there will be structural pressures for ongoing government spending and investment that will be supportive of near-term growth.

The benefits of technology, such as generative AI, are likely to be material. And the significant investments being made in capex and new business models, as well as in the green transition, will support growth. It is striking that the US has, by far, the best post-pandemic economic performance – and is the most advanced on these dimensions: significant industrial capex, leading on new business models, and pioneering the development and deployment of new technologies.

Indeed, it is increasingly clear that the global economy is moving out of a secular stagnation regime into an environment of higher trend growth, higher inflation, and higher rates. This provides some ground for some optimism that the post-pandemic decade will be different from the post-global financial crisis decade. Growth in investment and total factor productivity may be higher than forecast. Reindustrialisation across many advanced economies will be positive for the economic outlook.

The early productivity data in the US and several other leading economies is looking more promising than after the global financial crisis. And I continue to place weight on some of the emerging positive dynamics, from technology to increased investment rates. Indeed, advanced economy growth has been surprisingly resilient over the past couple of years.

But supporting policies and firm behaviour will be required to capture this economic potential: investment in capital and innovation, development and deployment of technology, and so on. The US is providing a sense of what is possible. Of course, the US has policy degrees of freedom that smaller economies don’t have. But leading small economies (such as Singapore) are investing heavily in technology, skills and innovation, are moving into new high growth sectors, and so on.

In an era of strategic competition between geopolitical rivals, differences in trend growth rates will have geopolitical implications. Over the past year, the US has been growing rapidly – strengthening its strategic position. In contrast, economic weakness can compromise geopolitical heft (China, Europe). Many governments, large and small, understand this relationship – and are beginning to respond. For example, this impulse has at least partly motivated the ambitious recommendations from the upcoming Draghi report on strengthening EU competitiveness, along with this week’s Letta report.

There are meaningful risks ahead, from geopolitical disruption to financial instability and the increasingly evident costs of climate change. But the incoming data, the early signs of positive policy responses, and technology developments, provides grounds for optimism about productivity moving onto a stronger path. An interesting analogy is to the bumpy 1980s that preceded the productivity surge from the mid-1990s. The economic outlook for this decade may be quite different than the pre-pandemic decade.

These notes provide a sample of the global insights and advice that we provide to clients. There are a few ways you can work with us:

§ Schedule a presentation or workshop: I can bring distinctive insights on global macro, geopolitics, and policy to your next event

§ Access tailored insights: We provide briefings and advice, focused on understanding the practical implications of global developments and options for navigating these dynamics - on a project or retained basis.

§ ‘Chief economist for hire’: We can provide an embedded source of strategic counsel, providing a cost-effective way of strengthening strategic capability in your organisation.

Do get in touch with me at david.skilling@landfallstrategy.com for information on these services and options for how we can support you.

If you haven’t already, you can subscribe for free to receive my public notes.

If you liked this note, please hit the like button and also share it with your network:

Previous small world notes are available here:

You can also connect with me on LinkedIn.