Currency wars?

Currency wars?

The strong USD is generating economic pressures around the world, with the potential for disruptive responses – reinforced by geopolitical rivalry

FYI, I am turning off the paid subscription option for these notes next week, and will be bundling this paid analysis into my broader client advisory services. I plan to continue to write regular free notes - like today’s - and there will be no change for free subscribers. Thanks to all for your ongoing interest in these notes. And please do get in touch for more information about our global economic and geopolitical advisory services – details follow at the bottom of this note.

Pressures on exchange rates are emerging across the global economy as central banks move at different speeds in changing policy rates.

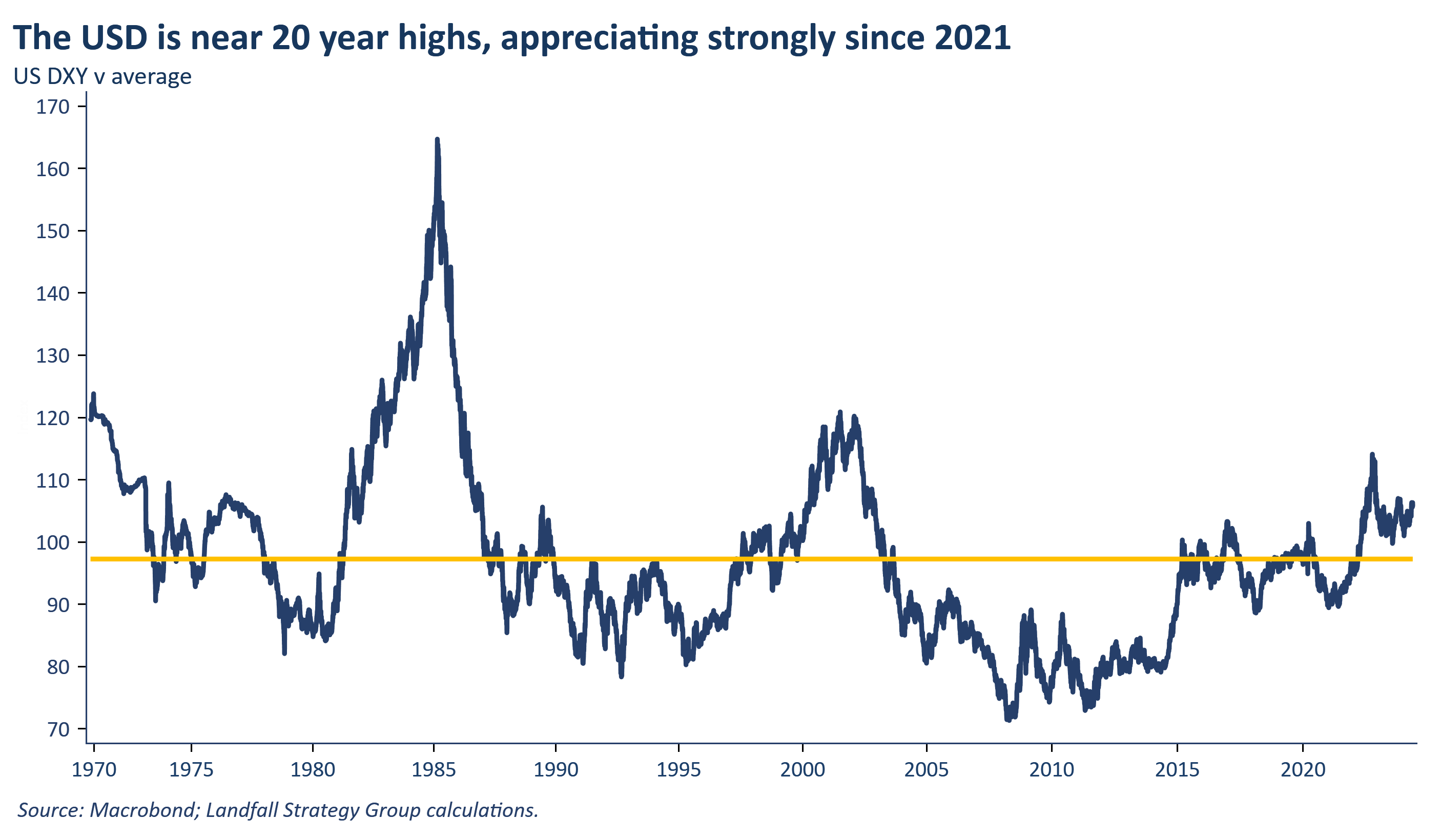

The US dollar index (the DXY) has been at levels not seen since 2002, with many major currencies sitting at low levels against the USD. USD strength is likely to persist because inflationary pressures are proving persistent in the high pressure US economy. The likelihood of material policy rate cuts by the Federal Reserve in 2024 has diminished rapidly.

The centrality of the USD in the global system (~90% of global payments and over 60% of official reserves) means that this will have meaningful economic and geopolitical spillovers.

Our currency, your problem

For emerging markets, a high rates, high USD environment raises the risk of capital outflows and financial instability as well as pressures on borrowing costs. And a strong USD acts as a headwind to world trade growth because so much of world trade is invoiced in USD.

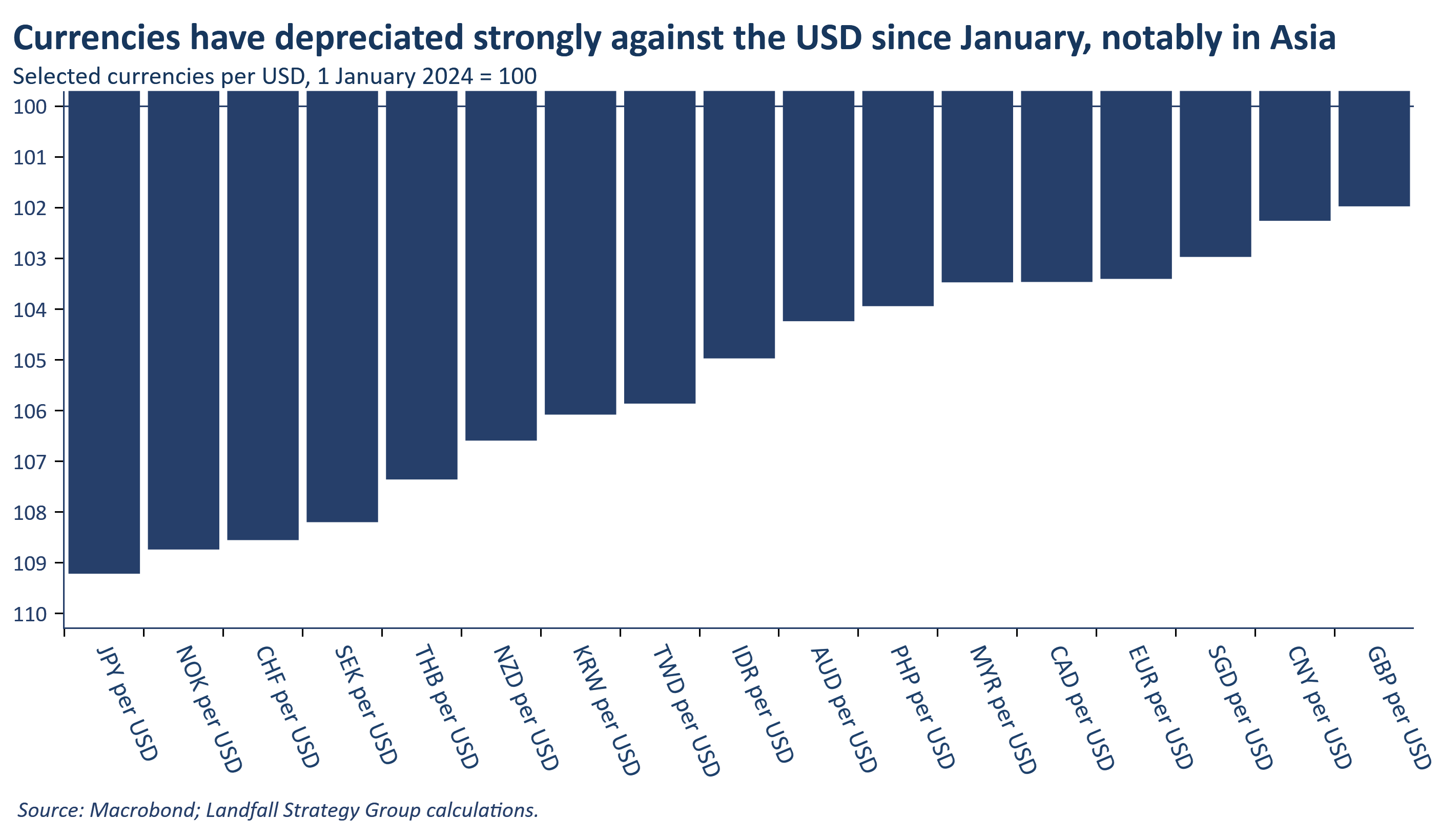

Specific economies are being materially impacted. For example, the euro and sterling are under downward pressure because the ECB and Bank of England are expected to cut policy rates more rapidly than the Federal Reserve. Some are forecasting euro parity with the USD, which hasn’t been seen on a sustained basis since 2002. This would make exports from European countries more competitive, but would make the disinflationary process more challenging. And despite ECB denials, the changed Fed stance will likely slow the pace of rate cuts by the ECB to avoid rapid depreciation.

The pressures are even more acute elsewhere, notably in Asia. Despite the Bank of Japan lifting the policy rate out of negative territory in March, the yen has depreciated by ~15% over the past year. It fell to ~160 to the USD earlier this week, a 34-year low, before recovering to ~153 on Thursday (partly on official interventions in the market to support the currency). Japanese officials are concerned because a weak JPY reduces the purchasing power of Japanese firms and citizens – and creates additional inflationary pressures.

Other Asian currencies are under pressure, notably in South Korea. Indeed, last week the US, South Korea, and Japan issued a rare joint statement expressing ‘serious concerns’ about ‘the recent sharp depreciation of the Japanese yen and the Korean won’. And many ASEAN currencies (ex SGD) have depreciated substantially: the Indonesian central bank raised rates recently, partly to offset these pressures.

Asian economies and financial systems are in much better shape than during the Asian financial crisis, and floating exchange rate systems are more resilient. Even so, there are risks of capital outflows and associated financial instability,

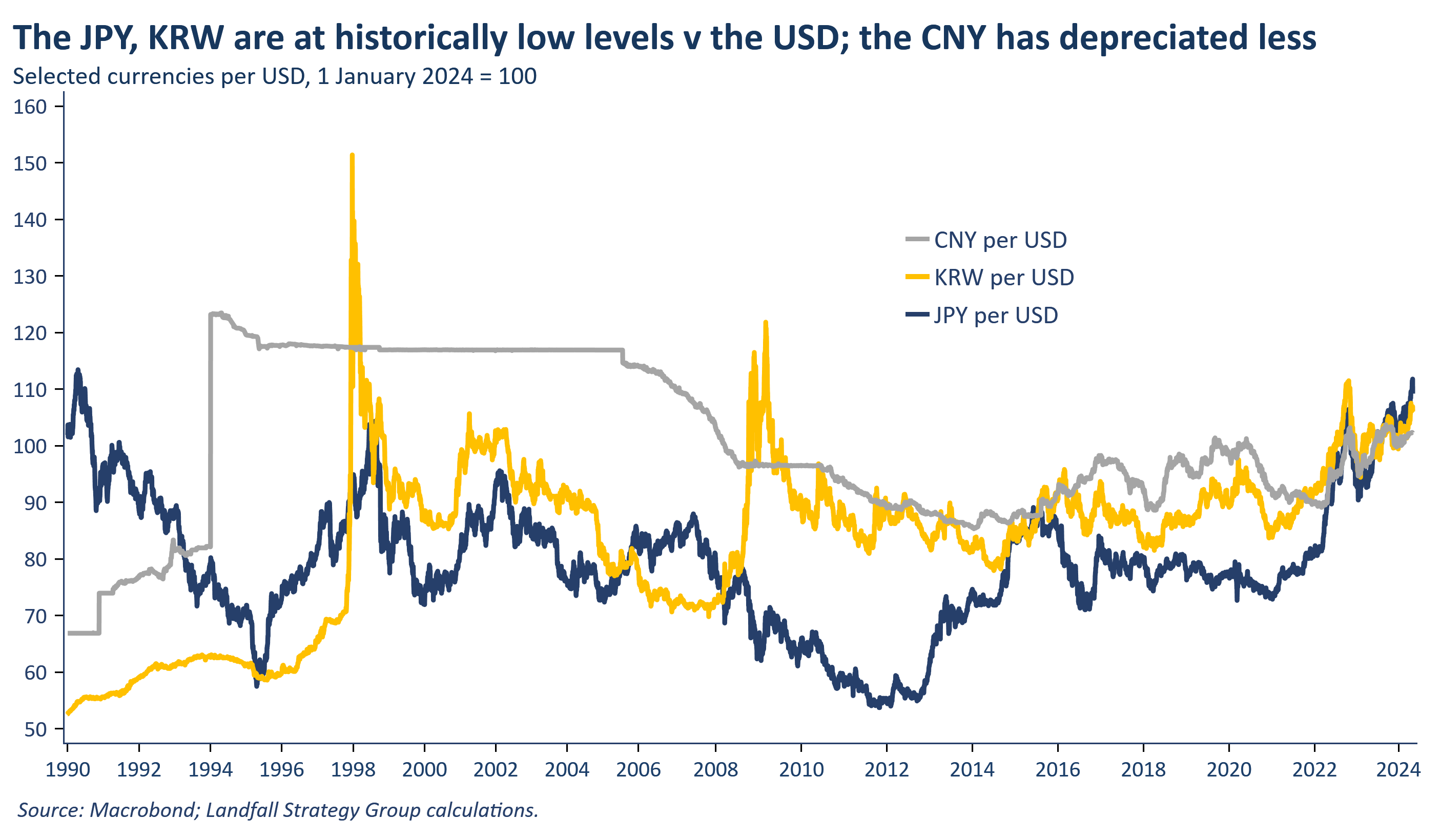

And the variation in extent of depreciation against the USD is reshaping the competitive landscape for Asian firms. For example, the depreciation of the JPY against the KRW and CNY is helpful for the competitive position of Japanese firms.

China’s currency has depreciated only modestly (~2%) against the USD since the start of 2024, due to its exchange rate arrangements: the CNY is managed against a basket of currencies, of which the USD is the most important. This means that China is importing tight monetary policy from the US: contributing to China’s low/negative CPI/PPI inflation and to muted GDP growth.

Sustained USD strength will impose a range of economic and political costs around the world, which will intersect with geopolitical tensions. Policy-makers will face incentives to respond, and large economies may treat exchange rates as part of broader strategic competition. So although the economics suggest a period of sustained USD strength, firms, investors, and policy-makers should also position for policy-induced exchange rate turbulence ahead.

The biggest near-term risk is for uncoordinated changes to exchange rate policy by the big powers, in particular the US and China. Over time, the strong USD will impose more evident costs on the US economy – less competitive exports and a likely larger US trade deficit, as well as making it more expensive for foreign firms to invest into the US. These costs are not persuasive to the Fed. But Mr Trump and his advisers (such as Robert Lighthizer) seem to take another view: Mr Trump has called USD strength ‘a disaster’, with apparent sympathy for a deliberate depreciation of the USD.

In a recent note, I discussed the potential threat to US macro policy institutions in a second Trump Administration. In office, he might act differently – but a deliberately weakened USD alongside higher tariffs is possible. This would have echoes of President Nixon’s unilateral departure from the Bretton Woods arrangements.

‘The dollar is our currency, but it's your problem’, US Treasury Secretary John Connally (1971)

Exchange rates & global economic fragmentation

Perhaps even more disruptive is the potential for China to shift away from its exchange rate policy, in place since 1994, in which substantial depreciation against the USD is prevented. There are economic costs for China associated with the status quo, as it imports tight US monetary policy in the context of a sluggish economy and very high debt levels. Allowing for a devaluation of the currency, or moving to a more flexible exchange rate regime, are possible options – which would also support China’s broader decoupling agenda, as it reduces exposure to the US on multiple dimensions. And it would support China’s drive for export-oriented growth.

Some are seeing signs of China preparing for a devaluation (gold purchases, stockpiling behaviour). I think a big bang change is still a relatively small probability (say 10-20%), but it would be a global earthquake if it did occur. In addition to the risk of capital outflows from China, it would lead to cascading exchange rate realignment across Asia.

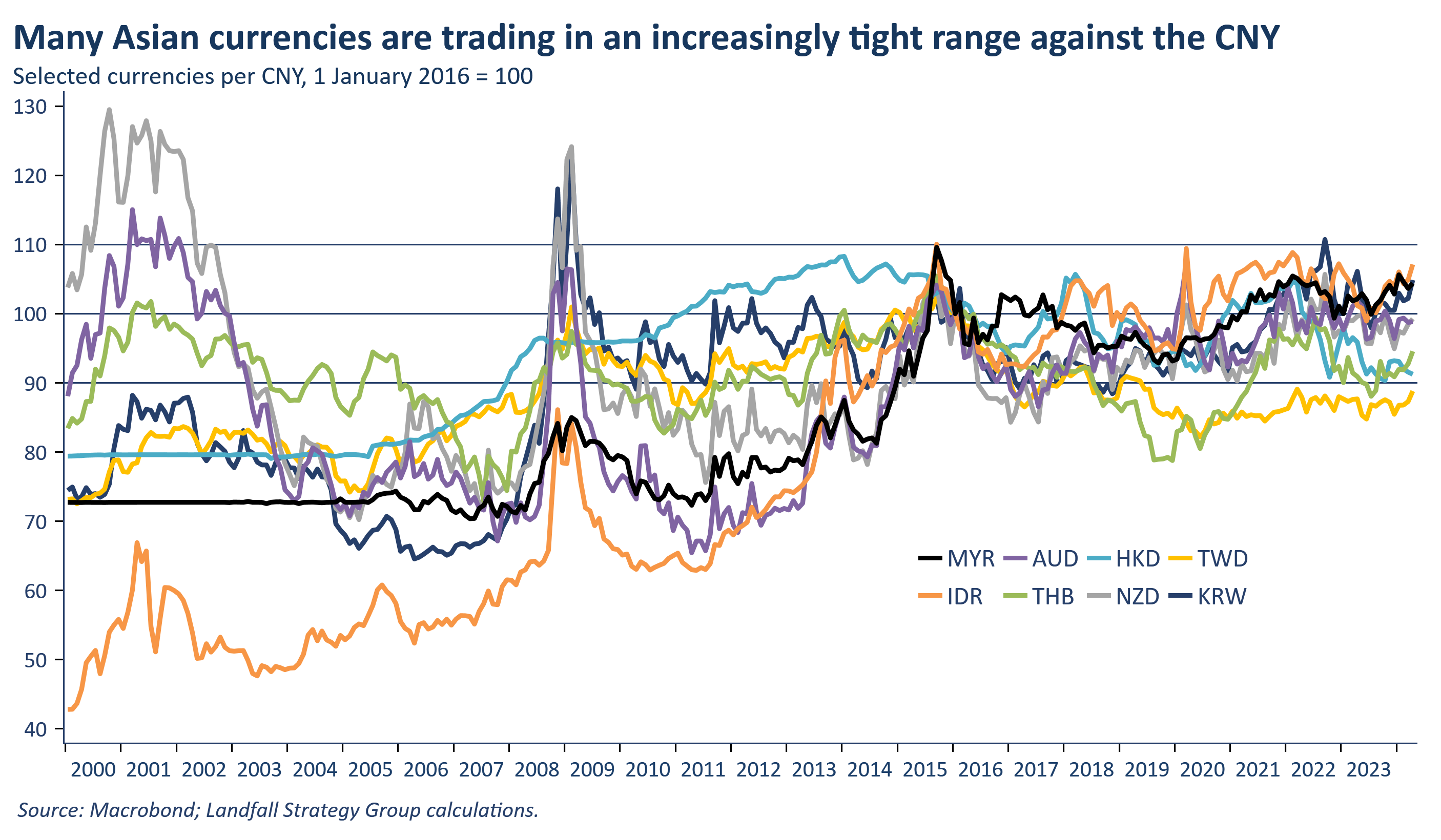

Over the past decade, many Asian currencies have traded in an increasingly tight range against the CNY – reflecting the economic importance of China in the region. A Chinese exchange rate shift would lead to a disruptive reaction as other countries tried to preserve their competitive position.

And given China’s central role in the global trading system, this would lead to substantial spillovers across the global economy. Currency wars could become a more evident part of global economic fragmentation: given the size of China’s trade surplus (particularly in manufacturing), other economies would not stand still.

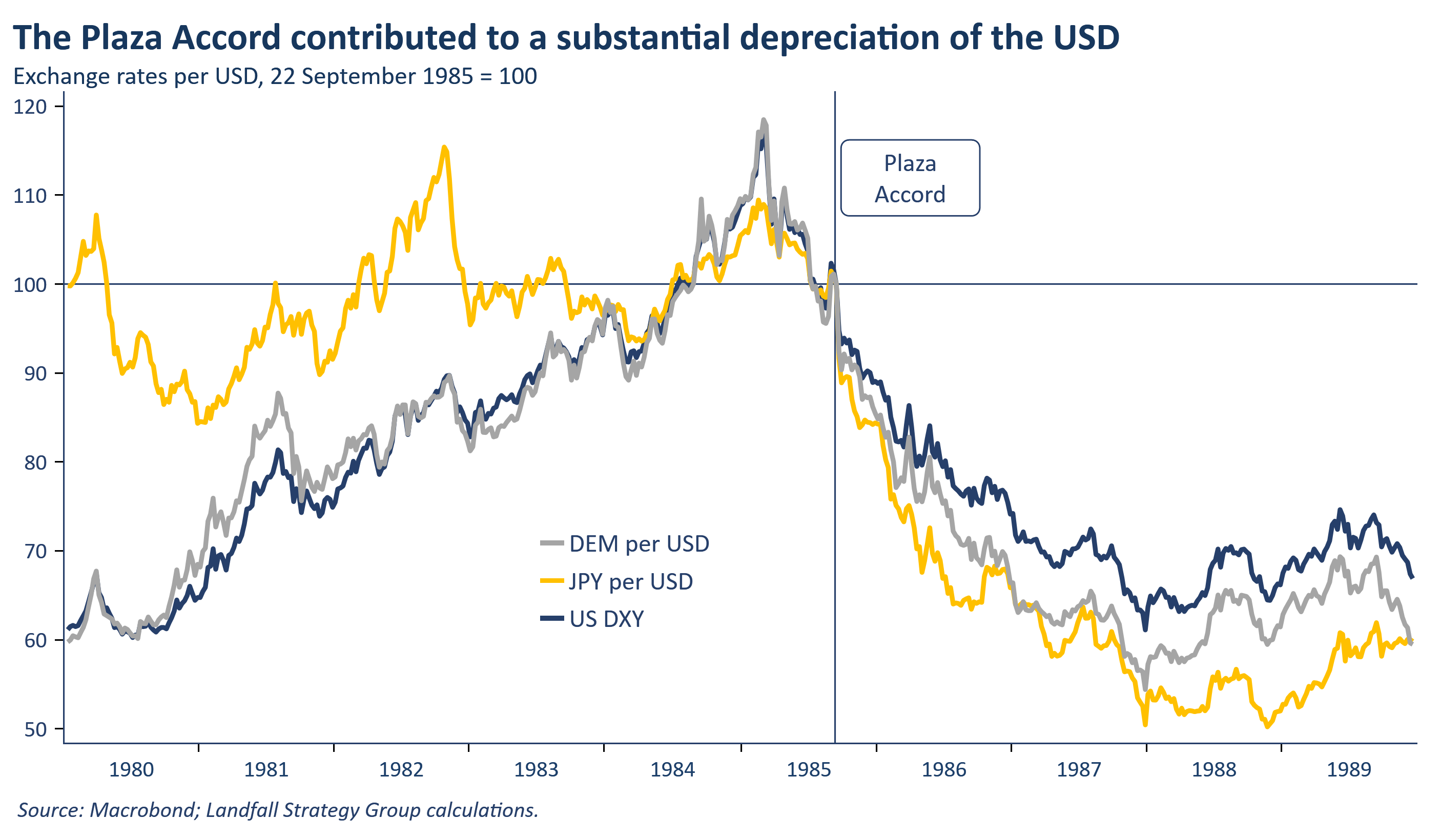

One other scenario is for a managed realignment of currencies, as happened with the Plaza and Louvre Accords in 1985 and 1987 – a response to a strong USD and a weak JPY and DEM (Deutschemark). This coordinated programme of intervention led to a significant revaluation of currencies, in the context of US concerns about strategic competition and the trade deficit. It is difficult to see sufficient trust and incentive alignment for this to proactively happen in a collaborative manner in the current environment (e.g. at the G7 or G20). But it may come in response to threats (e.g. US tariffs) and after unilateral action.

Short of this, the strong USD will reinforce geopolitically-motivated efforts to reduce exposure to the USD: ongoing efforts at de-dollarisation of invoicing/payments, official reserves, as well as exchange rate arrangements (perhaps Hong Kong). Even so, this will be a gradual process: the USD will be hard to dislodge.

The economic stresses of a strong USD have the potential to lead to global economic and financial instability as countries respond. At least part of this response will be motivated by geopolitical considerations, leading to further fragmentation of the global economy. Exchange rate arrangements and policy are partly a technical economic choice, but also reflect geopolitical dynamics. After a period of global inflation shocks, watch for increased turbulence in key exchange rates.

These notes provide a sample of the global insights and advice that we provide to clients. There are a few ways you can work with us:

§ Schedule a presentation or workshop: I can bring distinctive insights on global macro, geopolitics, and policy to your next event.

§ Access tailored insights: We provide briefings and advice, focused on understanding your specific exposures to global dynamics and options for capturing opportunities and managing risks.

§ ‘Chief economist for hire’: We provide an embedded source of strategic counsel, providing a cost-effective way of strengthening strategic capability in your organisation to navigate through a changing world.

Do get in touch with me at david.skilling@landfallstrategy.com for information on these services and options for how we can support you.

If you haven’t already, you can subscribe for free to receive my notes.

If you liked this note, please hit the like button and also share it with your network:

Previous small world notes are available here:

You can also connect with me on LinkedIn.