No summer calm...

The (northern) summer has been dominated by political and economic turbulence; expect more to come

My plans for a relaxing Greek holiday from mid-July were partly thwarted by a particularly volatile few weeks of economic and political news.

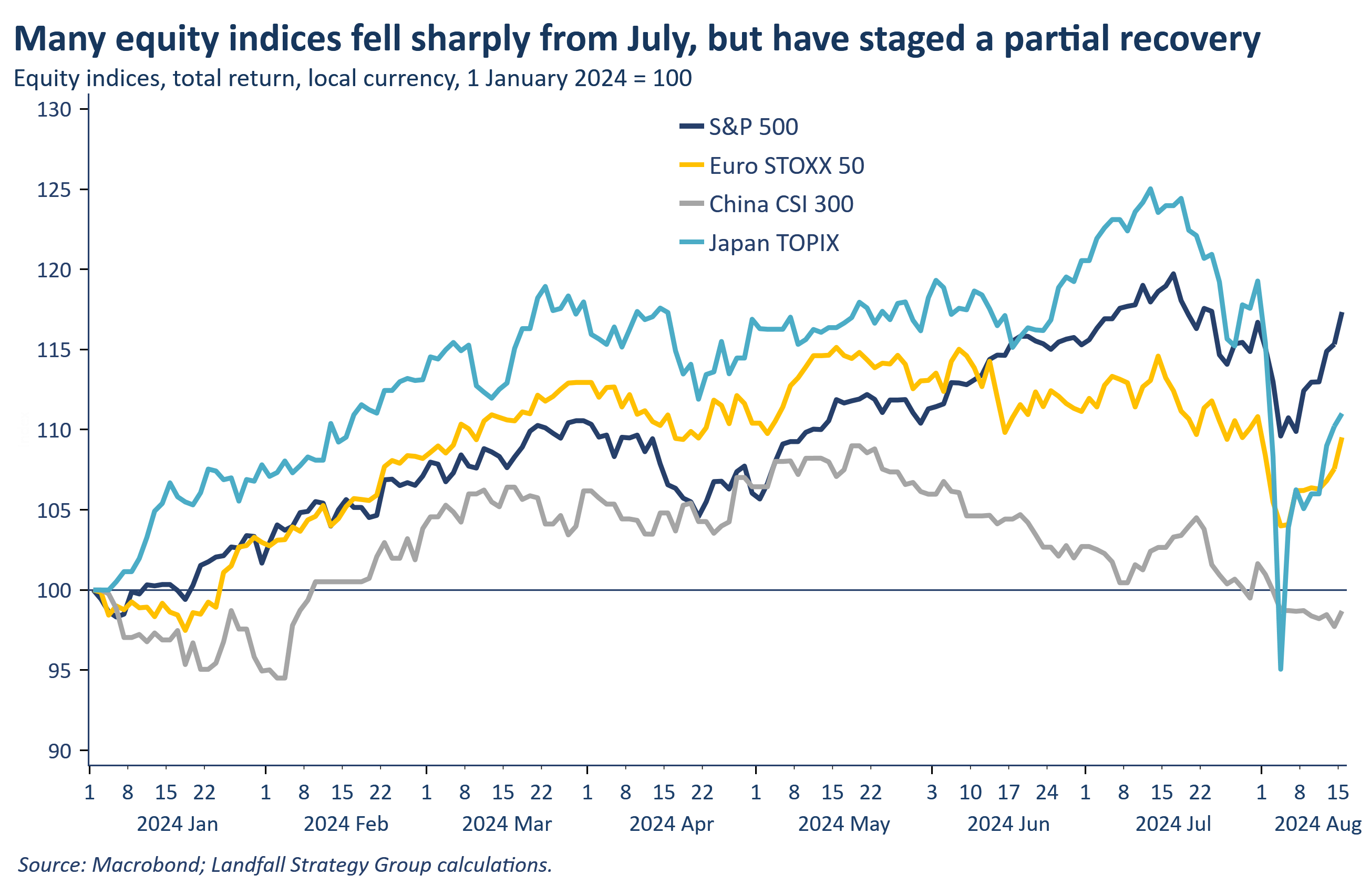

Equity markets sold off sharply on concerns about US recession, an AI bubble, as well as the unwinding of the Japanese carry trade on an appreciating JPY (and various other reasons). A recovery has since clawed back about some of these losses, notably in the US, but markets remain jittery. Elsewhere, one US Presidential candidate was shot at and the other stepped down from the race; the race dynamics have been completely reset by the candidacy of Kamala Harris. And there were riots across the UK; China continues to equivocate on economic policy; and risks of military escalation in the Middle East are rising.

Beyond the near-term drivers, this volatility reflects regime change in the global system: macro policy ‘normalisation’ in key economies alongside new macro behaviours (structurally higher inflation and rates); ongoing political realignment…