Election risk ahead

Election risk ahead

Recent market volatility after elections illustrates the economic importance of political institutions; with implications for the US Presidential election

Geopolitical risk is rising around the world. But domestic political and institutional risk is on the rise also, in response to structural economic challenges and political polarisation.

One of the major themes of 2024 is that it is a year of big elections; see our 2024 outlook note. And almost halfway into 2024, the consequential nature of these elections is clear – both politically and economically. The experience of the past fortnight is instructive for thinking about the impact of the major elections remaining this year, most notably the US Presidential election.

Emerging markets

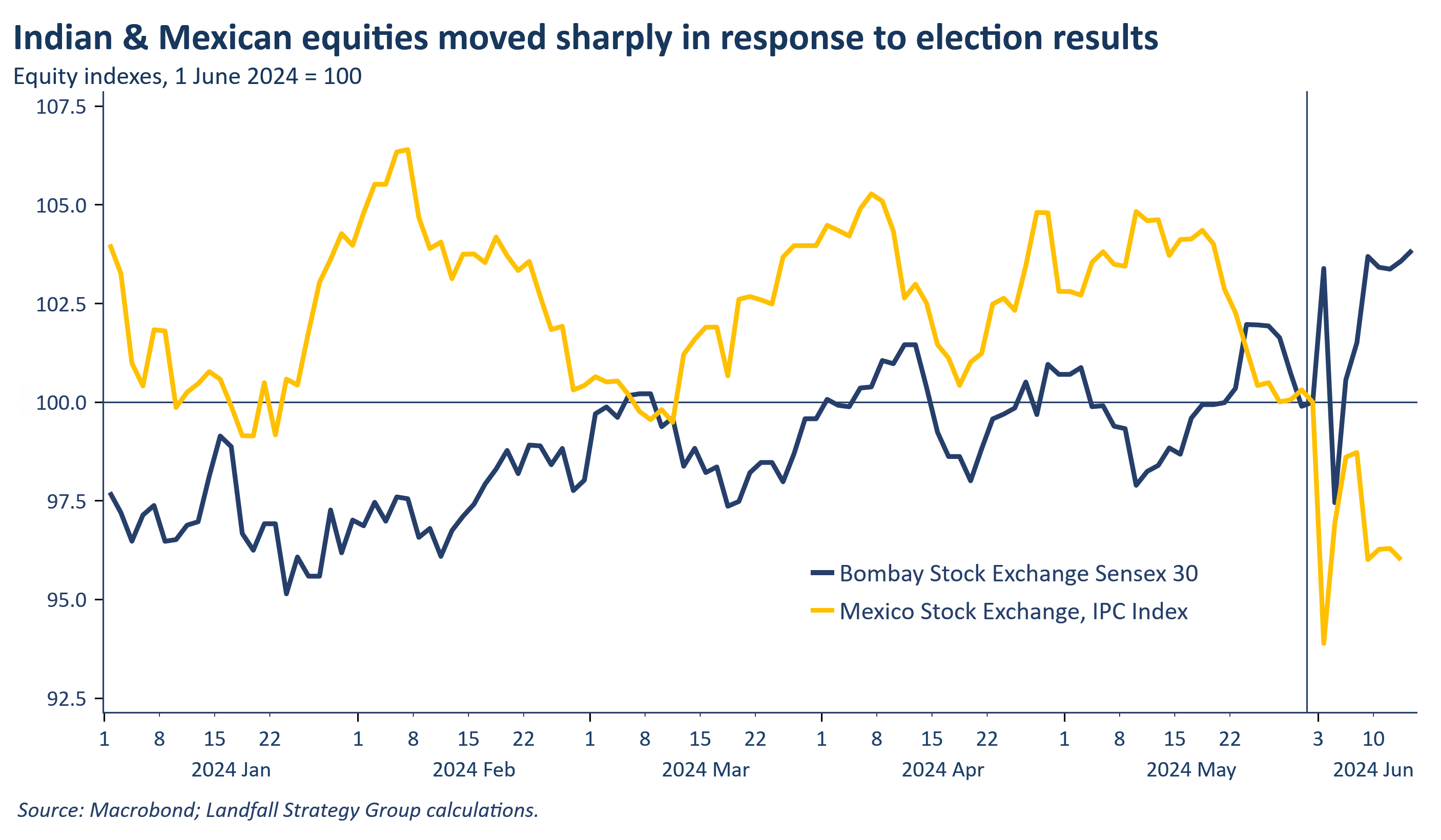

Last week, markets responded violently to election results in India and Mexico. In India, the world’s largest democracy, equities first surged on (wildly inaccurate) exit polls that suggested a strong result for PM Modi’s BJP; and then sank when it turned out that the BJP had lost seats and would have to govern in a coalition. Investors – domestic and foreign – are positive about the policies that PM Modi has implemented, which have helped India to become one of the fastest growing emerging markets – and attracted significant capital.

The reduced BJP vote share – partly reflecting voter concerns about sectarian and authoritarian tendencies – and the accompanying constraints on governing were initially interpreted negatively. But markets are now trading higher than immediately prior to the election, on a view that reforms are likely to continue – and that institutional constraints may be good for the quality of policy.

The economic importance of political institutions can also be seen in Mexico. Claudia Sheinbaum, the successor to President Andres Manuel Lopez Obrador, won a stronger than expected vote share. And her Morena party also won a supermajority in the House as well as control of the Senate. The absence of meaningful institutional checks and balances because of this strong result reinforced concerns in the business community about the policy outlook – and the risks to the Mexican growth model. There will be less ability to oppose policies that weaken the business environment and that compromise other institutions (such as judicial independence).

Mexico has been one of the better-performing equity markets globally, as it positions as a production hub close to the US (see my last note). But investor concerns about the quality of policies and institutions under the new President led to equity markets immediately selling off by ~6%; and they remain down a week after. The Mexican peso is down by ~10% against the USD since the election.

The market reaction to these elections shows that political institutions matter: markets care about the ability of the government to pursue a credible, coherent economic programme as well as adherence to political institutions. Strong institutions are valued by markets. Strongman leadership can generate good economic outcomes for a period, but the distribution of outcomes increases markedly: poor outcomes become more likely in the absence of constraints.

Advanced economies

Traditionally political stability and institutional quality has been more of a concern in developing countries; there is often a risk premium on investing into emerging markets. But there is increased concern about political institutions and state capability in advanced economies; in 2019, I wrote that the world is ‘becoming an emerging market’ with a broad weakening in political institutions.

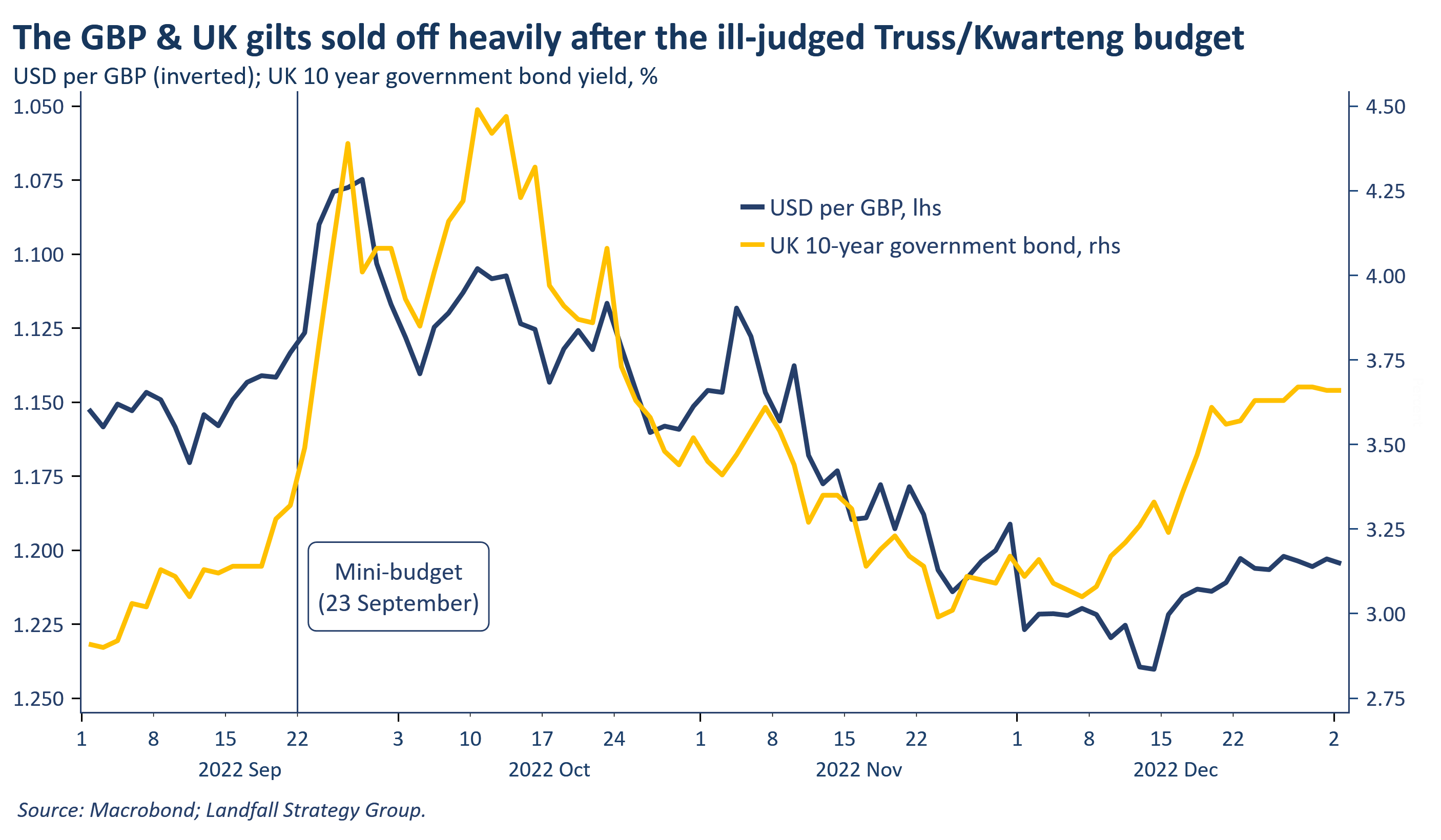

The re-rating of the UK after the Liz Truss mini-budget in 2022 was a good example of these institutional risks. In contrast, markets are comfortable with the (almost certainly) incoming Labour government: Labour are >20 points ahead in the polls. Business polling is generally positive on Labour: greater institutional stability and policy competence is expected after several post-Brexit years of challenging key institutions (the judiciary, Parliament) as well as policy chaos.

Last weekend’s European Parliamentary elections provide another example. At an EU-wide level, the political centre held. Although the parties on the far-right won seats, they did not do as well as had been expected a few weeks back, and the centre-right EPP grouping won seats. There will be an increased focus on economic competitiveness, migration, and geopolitical issues – and likely less focus on environmental issues.

But at a country level (such as France and Germany), these election results have weakened incumbents and sparked uncertainty about the coherence and stability of national decision-making – which will have an impact on EU decision-making.

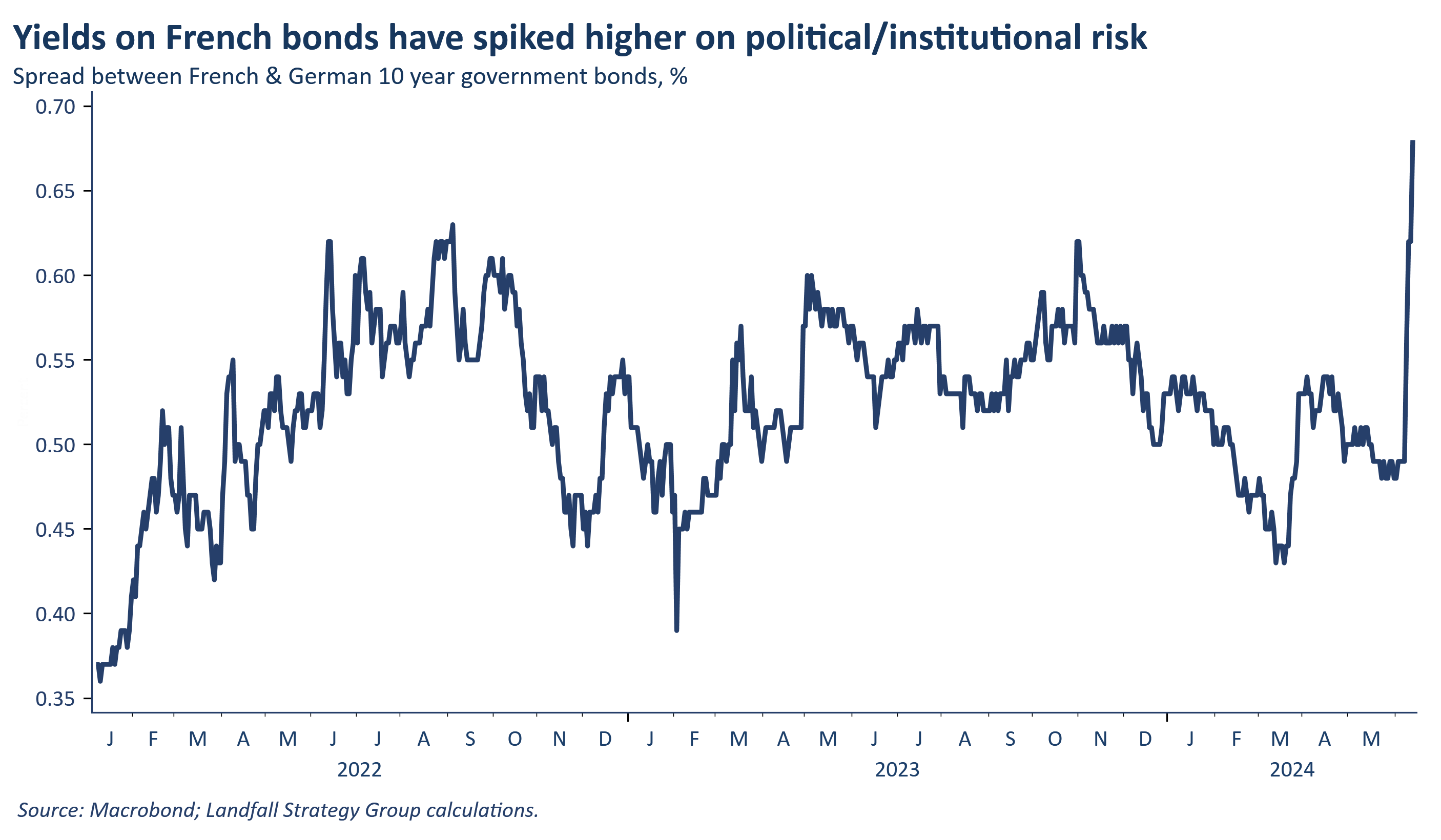

EU elections don’t normally rate much market attention. But these are not normal times for the EU, with increasingly evident structural economic challenges, political polarisation, as well as a confronting geopolitical environment. European markets sold off on Monday on higher risk and uncertainty, largely due to President Macron’s high-stakes decision to hold snap legislative elections in July. Markets are (rightly) concerned about the increased strength of Ms Le Pen; the Rassemblement National is polling well ahead of Mr Macron’s party.

These market concerns are not just about changes to tax rates or tighter regulation, but about the potential weakening of political norms and institutional functioning in France and across the EU. French equities and bonds have been under pressure; and the spread between French and German government bonds has spiked higher. Mr Macron is playing with fire, with potentially far-reaching consequences.

The lesson from these experiences is that firms and investors in advanced economies need to think much more about exposure to political and institutional risk – and particularly thinking about whether there are structural shifts underway. Policy risk clearly matters for firms and investors. But even more important is structural change in the integrity of political institutions (high quality government decision-making, independent civil service and macro policy institutions, rule of law, and so on). It is institutional risk that is being priced as much as specific policy risk.

Looking ahead

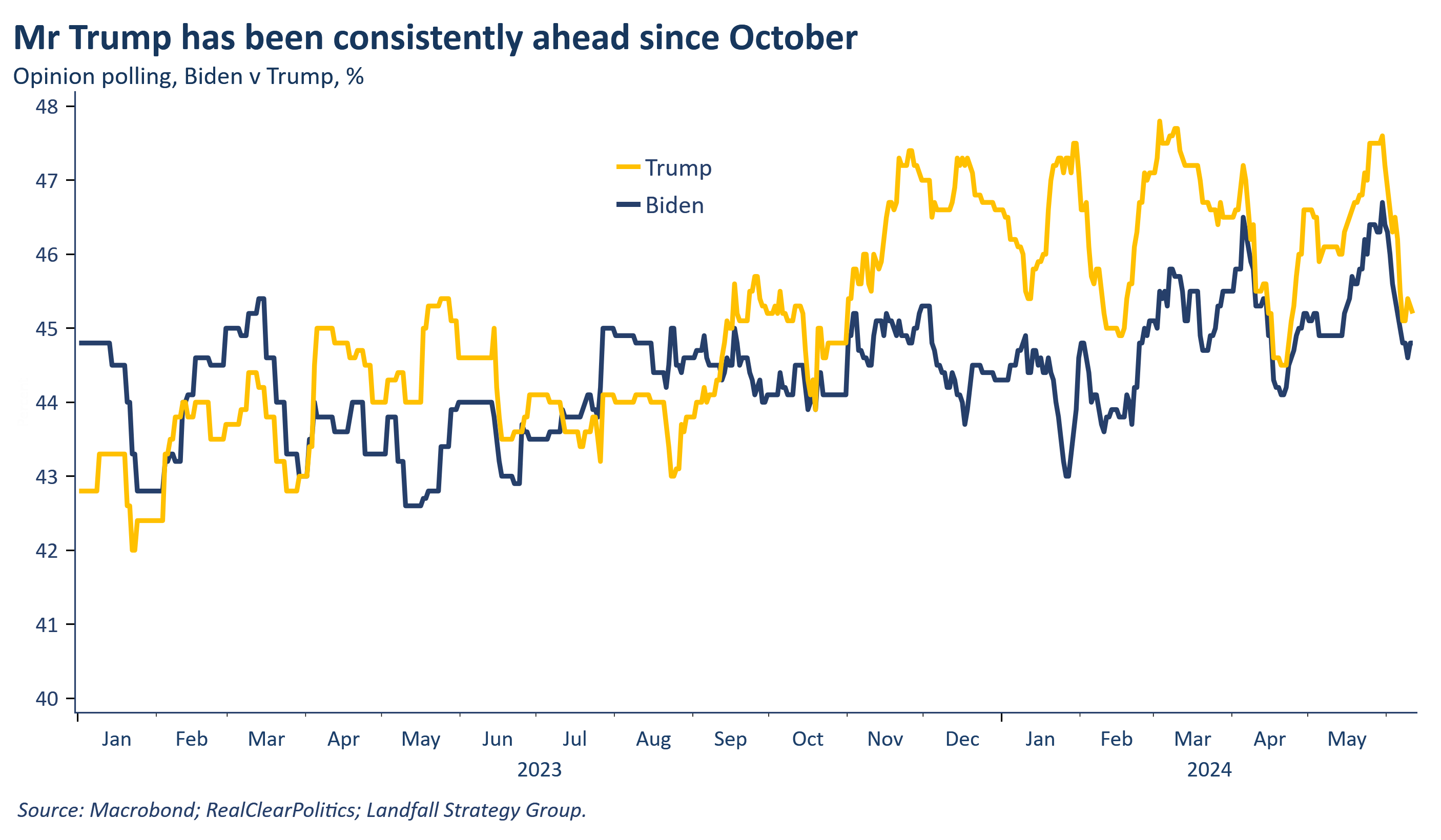

This recent experience has implications for assessing the risks associated with the biggest election of the year: November’s US Presidential election. Mr Trump remains ahead in most of the polls, but it is too close to call with confidence. For what it’s worth, I still think Mr Biden will edge it.

The big economic risks are not so much due to policy differences: there is a significant policy consistency between Mr Biden and Mr Trump, at least on economic issues and on China.

But this election is highly consequential for US institutions. Mr Trump has shown an unwillingness to be constrained by institutional constraints and norms. I recently discussed the significant risks around macro policy institutions in a second Trump Presidency – to a much greater extent than in his first term. From the independence of the Federal Reserve, to the way in which fiscal policy is implemented, expect to see institutions and norms being challenged. And of course there are broader risks around the functioning of democratic and judicial institutions.

Equity and bond markets performed well through most of the (pre Covid) Trump Administration, despite unconventional policies (such as tariffs). But it is not clear that this will be the case in the context of deeper institutional challenge. A ‘Truss shock’ in a US context is an increasingly plausible scenario on a combination of an unsustainable US fiscal path as well as weakening institutions.

Markets have been sanguine about these institutional risks, as have economic forecasts. But expect this to change as we move closer to the US election. Unlike the first Trump Administration, significant market turbulence is likely if he wins a second term.

In contrast, countries with strong political institutions and government legitimacy - as in many small advanced economies - are in an advantaged position.

If you find these notes valuable, you might be interested in accessing the unique insights and advice we deliver to our clients. We provide regular briefings to firms, investors, and governments on critical issues at the intersection of global economic and geopolitical dynamics; deliver presentations on global macro, geopolitical, and policy developments; and undertake commissioned analysis.

Please feel free to make contact at david.skilling@landfallstrategy.com to schedule an introductory call. We would be pleased to share some perspectives on global economic and geopolitical issues and discuss how our services can benefit you.

Related insights:

Escalating US fiscal risks, 5 April 2024.

Geopolitical shocks & shifts, 22 March 2024.

Scramble for supremacy: the world in 2024, 1 December 2023

If you liked this note, do forward it - or share it with your network:

Previous small world notes are available here:

You can also connect with me on LinkedIn.