Debt, rates, & balance sheet recessions

Rising rates will constrain governments’ fiscal space on high debt servicing costs and the need to offset reduced private borrowing

Fiscal space is a strategic asset in a wartime economy context. Increased government spending and investment will be needed on multiple fronts: increased military spending commitments, industrial and innovation policy, and the net zero transition, in addition to the increasing pressures from an aging population.

Without fiscal space, it will be difficult to engage in the investments required to engage in strategic competition. In this ‘wartime economy’, strategic competition will be waged by Treasuries as much as by Ministries of Defence.

Rising rates

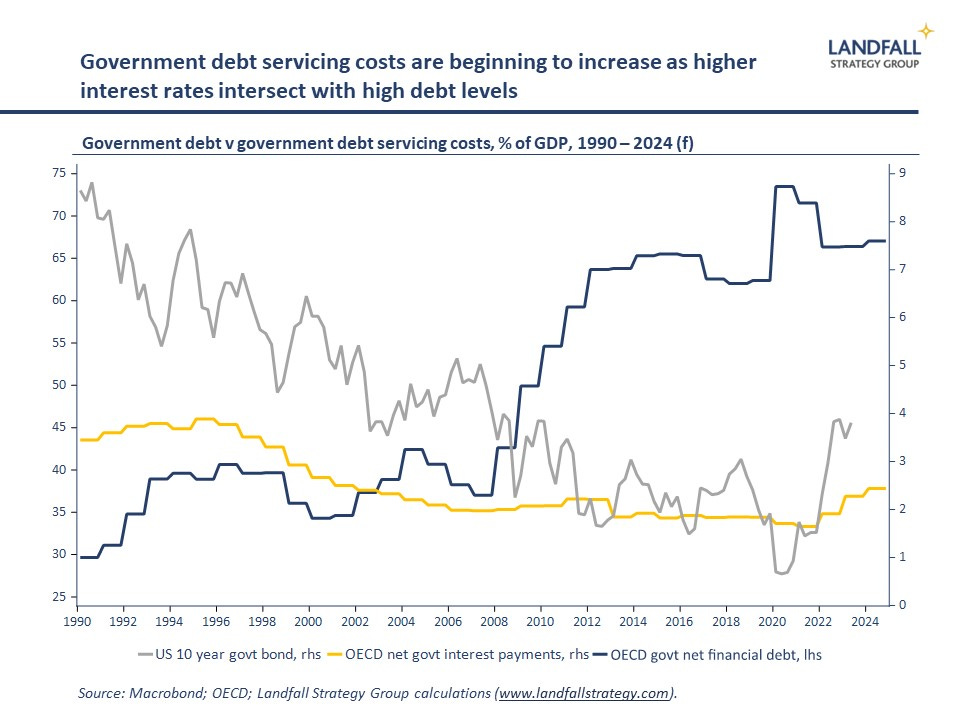

But this strategic competition will take place in the context of high public debt levels and higher interest rates. EU debt servicing costs are projected to double in 2024 relative to initial forecasts, squeezing government budgets; and there is a sharply rising trajectory of US federal debt servicing costs.

After years in which reduced rates have helped government finances, lowering debt servicing costs even as debt levels increased, the process is reversing. OECD net government debt was ~45% of GDP when interest rates were last at current levels, compared to >65% of GDP now. And whereas fiscal consolidation would ordinarily be expected on higher interest rates, strategic priorities will create pressure for higher public debt.

Governments with lower public debt levels will be in a better position to manage these pressures. However, there are exceptions: the US is able to attract foreign capital (the exorbitant privilege of being a reserve currency issuer); Japan’s low borrowing costs provide additional space; and eurozone membership enables high debt economies (Italy, Spain) to borrow more readily.

In general, smaller economies have markedly lower government debt levels. This greater fiscal discipline is because of their greater exposure to economic shocks (note the experiences of Ireland, Greece); they regard a fiscal buffer as important.

Ricardian equivalence redux

However, there are additional channels of fiscal policy exposure to higher rates than the level of government debt. Private sector debt (driven by corporate debt) has also increased over the past 15 years of low rates and QE. Across advanced economies, private debt is ~165% of GDP, and in China it is ~220% of GDP (having doubled since the global financial crisis).